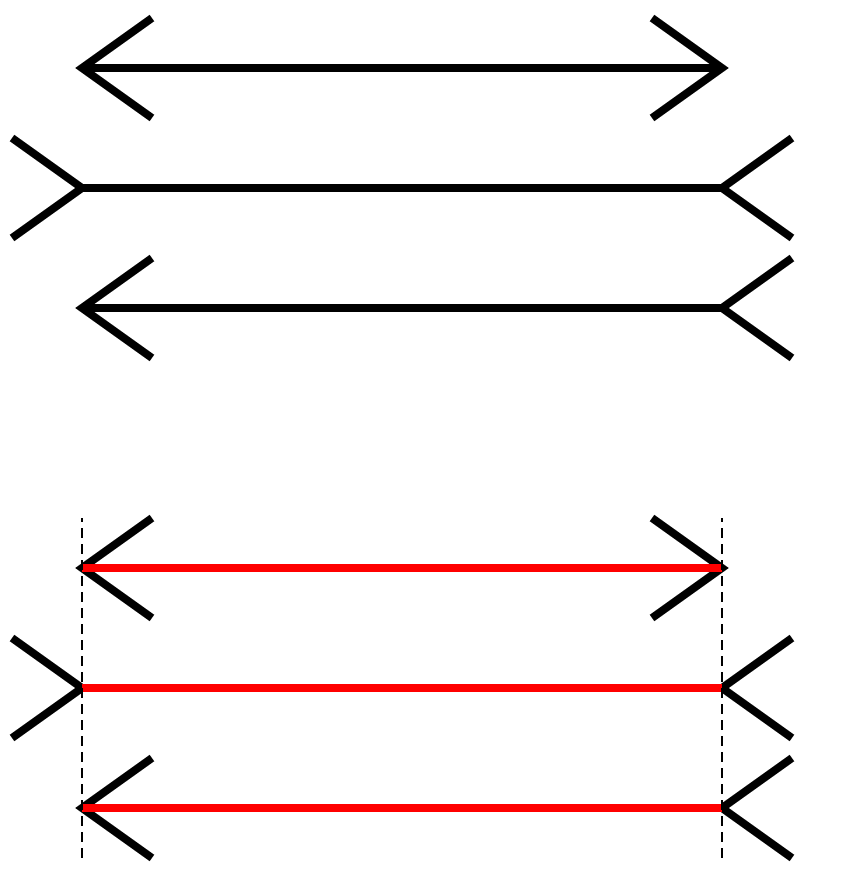

Many of us have seen the question in the accompanying graphic (the technical name of which is the “Müller-Lyer illusion”): Which of the lines is longer? When we look at them, we see that the lines in the middle (“arrow tails”) of each set are longer than the other lines (“arrows” and “arrowheads”), but we know that the two lines are equal. Even when we know that what we are seeing is an optical illusion, our eyes still tell us that the middle lines are longer!

Fibonacci / Wikimedia Commons

Much has been written about this optical illusion, but it was only recently that I had the pleasure of finding out why from Paul Slovic, an eminent University of Oregon psychologist who is among the originators of behavioral finance. Over a couple of drinks, Professor Slovic explained that while we might be embarrassed at thinking that the arrow tail lines are longer (even after knowing that the lines are equal), we should not feel so.

That’s because evolution has created our visual system in such a way that our brain compensates for distant objects (or objects that appear to be more distant), by giving them a different interpreted length. The arrow tail line is thus interpreted by the system that judges depth and perception as closer, and hence longer. This “heuristic” presumably was an adaptation that allowed us to make rapid and generally accurate judgments of visual perception.

The misinterpretation of the length of these lines is thus very likely a remnant of our survival mechanism. Even though we feel that the arrow tail line is longer, we know the lines are equal after we take out a ruler and measure them. Slovic was the first to document how our feelings significantly affect our decisions (this is known as the “affect” heuristic). In investing, as in other endeavors, one way to overcome our biases is to measure; i.e. use a ruler of some sort.

I have also recently written on how behavior can influence our perception of risk on the extremes. Not surprisingly, crises in particular, and surprises in general can influence our perception of risk on the extremes, something I witnessed firsthand as a portfolio manager trying to balance investor expectations of returns with downside and upside risk.

I have four main conclusions.

First, people generally feel better when they believe that they have portfolios with built-in insurance, i.e. protection against losses, even though the expectation (or average return) of a portfolio with or without such insurance is the same. This explains why people are willing to pay for insurance in the form of things such as put options even when they know that by itself, the insurance itself will surely be a loss. Witness the purchase of bonds around the world at negative nominal yields by investors, which guarantee a principal loss. But this behavior might not always be irrational or naïve.

Second, and a corollary of the first observation is that insurance, especially catastrophic insurance can remain expensive (and even get more expensive) if people feel (feelings again!), that the world is a dangerous place. Any arbitrageur who tries to take advantage of this without an infinite amount of capital is exposing himself to how fearful those feelings can get. The arbitrageur can sometimes just get run over by a fearful and stampeding herd.

And this fear can last for long periods. We only have to look at the very steep skew in the options markets (for example the difference of the implied volatility of far-out-of-the-money options against closer to at-the money options) to see that this fear premium has become a fixture of markets today. A behavioral perspective on the options markets shows that what drives this premium is the overweighting of subjective (or feelings based) probabilities for rare events like another financial crisis.

Third, and based on the research of some Yale economists, we find that it is not really fair to call the option buyer the “fish at the table” who is constantly paying out premiums to the “rational” seller of options, who is collecting sure profits. As a matter of fact, if we allow for behavioral biases (which can be persistent), both the buyer and seller of such insurance can be completely rational. This heterogeneity is what makes markets.

Fourth and final is the observation that people are prone to react to the “heat of the moment”, and can be time-inconsistent in their decision making process. In other words, they are likely to “feel” differently when they are in the middle of a crisis event than when they are in a quiet environment. A gambler with behavioral biases rationally stays too long at the table when losing and exits too early when winning. We simply cannot argue that this behavior is “wrong” and that the gambler is not executing a rational plan. This is just part of the survival mechanism.

Coming back to the length of the lines, it appears that for good reasons, how we feel can not only influence our vision, but also our investment decision process. And it also appears that one partial solution against the bias is to measure and quantify the magnitude of the distortions. How else can we explain the incredible swing in the equity markets over the last two months, which have gone from being down over 10 percent to now recovering almost all of their losses, without much changing fundamentally?

In this round, anecdotal evidence points to the quants, whose measurement-based methods appear to be winning over humans who are reacting to feelings. At least for now, the ability to measure and to not excessively react to feelings has proven to be a good approach for investing.

Why the Quants Might be Winning on Wall Street, Forbes

Vineer Bhansali, Ph.D. is the Founder and Chief Investment Officer of LongTail Alpha, LLC, an SEC registered investment adviser and a CFTC registered CTA and CPO. Any opinions or views expressed by Dr. Bhansali are solely those of Dr. Bhansali and do not necessarily reflect the opinions or views of LongTail Alpha, LLC or any of its affiliates (collectively, “LongTail Alpha”), or any other associated persons of LongTail Alpha. You should not treat any opinion expressed by Dr. Bhansali as investment advice or as a recommendation to make an investment in any particular investment strategy or investment product. Dr. Bhansali’s opinions and commentaries are based upon information he considers credible, but which may not constitute research by LongTail Alpha. Dr. Bhansali does not warrant the completeness or accuracy of the information upon which his opinions or commentaries are based.